When you’re choosing a health plan, it’s easy to focus on the monthly premium. But if you take even one regular medication, that number can be misleading. A cheap plan might leave you paying hundreds-or thousands-out of pocket for your prescriptions. The truth is, prescription insurance coverage isn’t just a bonus feature. It’s often the difference between staying healthy and skipping doses because you can’t afford your meds.

In 2023, 66.7% of U.S. adults used at least one prescription drug. That’s more than two out of every three people. And yet, a CMS survey found that 63% of people shopping for plans didn’t check if their specific medications were covered until after they’d already enrolled. By then, it was too late. You’re stuck with a plan that doesn’t cover your insulin, your blood pressure pills, or your monthly specialty drug-and you’re on the hook for the full cost.

What Exactly Does Prescription Coverage Include?

Prescription drug coverage is built around something called a formulary. That’s just a fancy word for the list of drugs your plan will pay for. But not all drugs are treated the same. Most plans split them into tiers, each with different costs.

Here’s how it usually breaks down:

- Tier 1 (Generic): These are the cheapest. Think ibuprofen, metformin, or lisinopril. Copays average $10.

- Tier 2 (Preferred Brand): Brand-name drugs your plan prefers because they’re cost-effective. Copays are around $40.

- Tier 3 (Non-Preferred Brand): More expensive brand drugs that aren’t on the preferred list. You’ll pay about $100 per prescription.

- Tier 4 (Specialty): High-cost drugs for conditions like cancer, MS, or rheumatoid arthritis. These often require coinsurance-meaning you pay 25% to 33% of the total cost. A single prescription here can run over $1,000.

Some plans also have a deductible before coverage kicks in. Bronze plans can have deductibles as high as $6,000. That means you pay 100% of your drug costs until you hit that number. Gold and Platinum plans usually have low or no deductibles, which makes them better for people on regular meds-even if the monthly premium is higher.

Key Questions to Ask Before You Sign Up

Don’t guess. Don’t assume. Ask these questions before you enroll.

1. Are my exact medications on the formulary?

This is the most important question. Not just the name-the exact brand and dosage. If you take 10 mg of lisinopril, but the plan only covers the 20 mg version, you’re out of luck. Use your plan’s online tool (or call them) and enter your medications by name. Don’t rely on general categories like “blood pressure meds.”

2. What tier is my drug on?

Knowing the tier tells you how much you’ll pay. If your drug is on Tier 3, you’ll pay triple what you’d pay for a generic. If it’s on Tier 4, you might be paying a third of the drug’s total cost. Ask: “Is there a cheaper alternative on a lower tier?” Sometimes switching to a similar drug can save you hundreds.

3. Do I need prior authorization?

Prior authorization means your doctor has to prove to the insurer that you need the drug before they’ll cover it. It’s common for specialty drugs and even some common ones. If you’re on a drug that requires this, expect delays. You might have to fill out forms, wait days, or even get denied. Ask your pharmacy or plan: “Does my medication require prior authorization?”

4. Is step therapy required?

Step therapy means you have to try cheaper drugs first-even if your doctor says they won’t work for you. For example, if you need a specific biologic for arthritis, the plan might force you to try three generics first. That can delay treatment and make your condition worse. Ask: “Do I have to try other drugs before this one is covered?”

5. What pharmacies can I use?

78% of Marketplace plans restrict you to a network of pharmacies. If you go outside it, you could pay 37% more. Check if your local pharmacy is in-network. If you use mail-order, confirm the plan covers it. Some plans only offer discounts if you use their mail-order service.

6. What’s my out-of-pocket maximum for drugs?

Some plans have a separate out-of-pocket limit just for prescriptions. Others combine medical and drug costs. If your plan has a $9,450 out-of-pocket maximum (typical for Bronze), that includes your drug costs. If you’re on a $5,000-a-year specialty drug, you could hit that limit fast. Ask: “Is there a cap on how much I pay for drugs each year?”

7. Are there coverage limits?

Some plans limit how many pills you can get per month. Others won’t cover refill requests until you’ve used up your last supply. If you take 30 pills a month, but the plan only allows 15, you’ll have to pay the rest yourself. Ask: “Are there quantity limits on my prescriptions?”

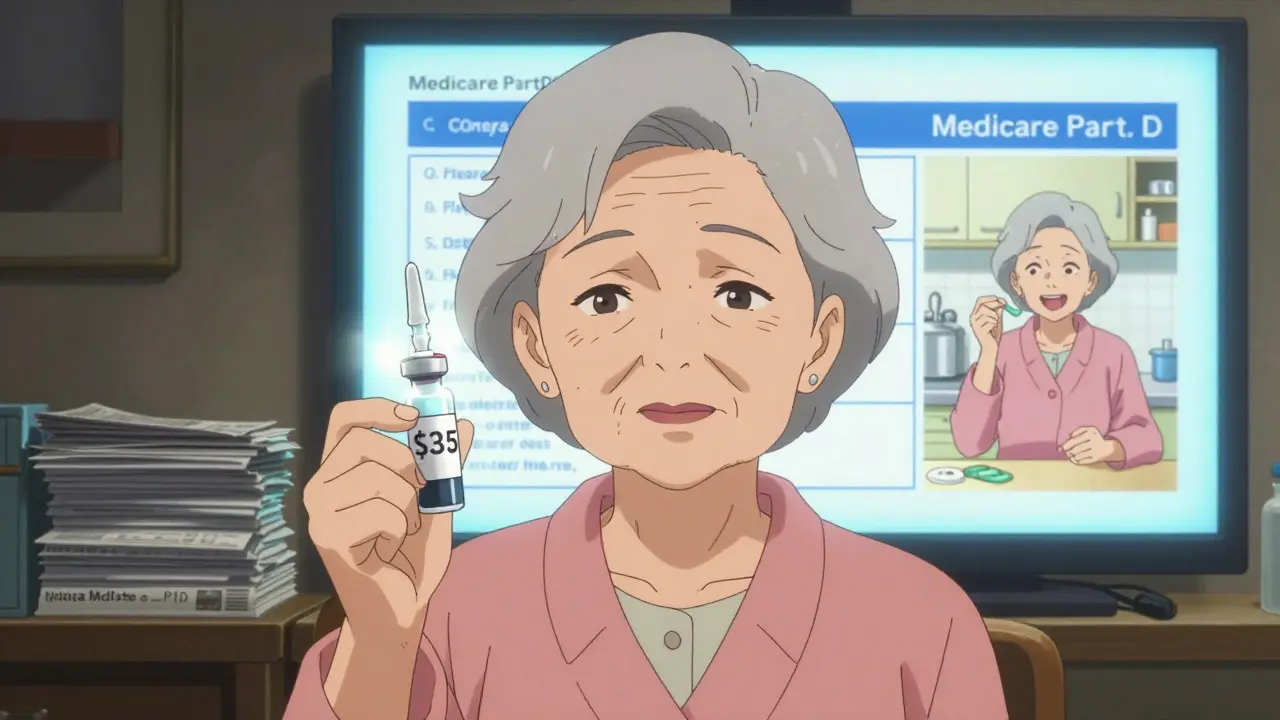

Medicare Part D: What You Need to Know

If you’re on Medicare, you have two choices: a standalone Part D plan or a Medicare Advantage plan that includes drug coverage. Both have formularies, but they work differently.

Standalone Part D plans had an average monthly premium of $34.70 in 2023. But 83% of them had a deductible. That means you pay full price until you hit that number. The coverage gap (“donut hole”) still exists in 2024-you pay 25% of drug costs between $5,030 and $8,000 in total spending.

Starting in 2025, everything changes. The Inflation Reduction Act caps your out-of-pocket drug costs at $2,000 per year. Insulin will cost no more than $35 per month. And the donut hole disappears. But until then, you need to be smart.

Compare plans using the Medicare Plan Finder. Enter your exact drugs and dosages. Don’t rely on the “lowest premium” filter. A plan with a $10 monthly fee might have a $450 deductible and not cover your drug at all. That’s not a deal-it’s a trap.

When to Act

You only get one shot each year to change plans without penalty.

- Marketplace plans: Open Enrollment runs from November 1 to January 15. Use the plan comparison tool. Enter up to 15 medications and 3 pharmacies. The tool will show you which plan saves you the most.

- Medicare: Annual Election Period is October 15 to December 7. Use Medicare.gov’s Plan Finder. Enter your drugs by NDC code (you can find this on your pill bottle or ask your pharmacist).

People who spend 20+ minutes checking their drug coverage save an average of $1,147 per year. That’s more than the difference between a Bronze and Gold plan. If you’re on regular meds, this isn’t optional. It’s essential.

Real Stories, Real Costs

One user on Reddit shared: “I thought my Silver plan covered my $4,200/month specialty drug. Turns out, there was a $500 copay cap. I got billed $3,700 in one month. I had to dip into savings.”

Another, on Medicare forums, said: “I switched from a low-premium Part D plan to a Gold-tier Advantage plan. My insulin went from $120 to $20 per month. The $200 higher premium? Worth it. I saved $8,400 a year.”

These aren’t rare cases. In 2023, 32% of Medicare Part D beneficiaries switched plans-mostly because their meds weren’t covered or cost too much.

What’s Changing in 2025 and Beyond

The biggest shift is the $2,000 annual cap on out-of-pocket drug costs for Medicare Part D. That’s huge. But it’s not the only change. Medicare will start negotiating prices for 20 high-cost drugs starting in 2026. Experts predict premiums could drop 10-15% by 2030.

Private insurers are also shifting. By 2026, 70% of new Marketplace plans are expected to use “value-based insurance design”-meaning they’ll lower copays for drugs that treat chronic conditions like diabetes or heart disease. That’s good news if you take those meds.

But there’s a looming problem: specialty drugs. Half of all new FDA-approved drugs in 2023 cost over $100,000 a year. Insurers are struggling to cover them. If you rely on one of these, keep checking your plan every year. Coverage can change fast.

Final Checklist

Before you enroll, run through this:

- ✅ List every medication you take, including dose and frequency

- ✅ Check if each one is on the formulary

- ✅ Find the tier and out-of-pocket cost

- ✅ Ask about prior authorization and step therapy

- ✅ Confirm your pharmacy is in-network

- ✅ Compare total annual cost-not just monthly premium

- ✅ Recheck every year. Formularies change.

Prescription drug coverage isn’t about saving a few bucks on your premium. It’s about making sure you can afford to stay healthy. The right plan doesn’t have the lowest monthly fee. It has the lowest cost for your drugs. Take 20 minutes. Ask the questions. You’ll thank yourself later.

In India, we don't have tiered formularies like this. Medicines are often sold over the counter, and insurance is rare. But I've seen people pay 30% of their income just for diabetes meds. This system? It's broken in its own way.

I just checked my plan. My insulin isn't covered. That's it. I'm done.

I didn't know about the pharmacy network thing. I've been paying extra to use my local CVS for years. That's $180 a year I could've saved. Ugh.

It's fascinating how we've turned healthcare into a labyrinth of bureaucratic tiered pricing. The fact that people must become actuaries just to afford their own prescriptions speaks volumes about the moral decay of our system. Truly, a tragedy dressed in corporate jargon.

I appreciate the thoroughness of this guide. As someone who manages chronic autoimmune conditions, I can confirm: the formulary check is non-negotiable. Last year, my plan dropped my biologic without notice. I had to appeal, submit three letters from my rheumatologist, and wait six weeks. I almost lost mobility. Don't wait. Document everything.

I just cried reading this. My mom had to choose between her blood pressure meds and her insulin last winter. She picked insulin. She lost 17 pounds. She's in the hospital now. This isn't about premiums. It's about people dying because they can't afford to live.

I spent 47 minutes on the Medicare Plan Finder last year. I entered every single medication-down to the 5mg vs. 10mg. I compared 12 plans. I printed out the results. I took them to my doctor. I switched. My out-of-pocket costs dropped from $8,900 to $1,100. I am not exaggerating. This is life or death. You must do this. Do it now. Do not wait until you're in crisis. Do not wait until your pharmacy calls and says, 'We can't fill this.' You have power. Use it.

I didn't know about the 2025 cap! 😭 I'm so glad I'm on Medicare now. My husband's rheumatoid arthritis meds used to cost $2,200/month. Now? $35. I cried when I saw the new card. Thank you for this info. I'm sharing it with everyone I know. 🙏❤️

so i just realized my plan covers my med but only if i use mail order? like i have to order 90 days at a time? i hate that. i can't even get it at my local walgreens? and now i have to wait 2 weeks? what the actual f. also i spelled mail wrong. whoops.

This is one of those topics where the system is designed to confuse you. But you don't need to be an expert. Just do the 20-minute checklist. Write it down. Use the tools. You're not lazy if you need help. You're smart if you ask. And if you're helping someone else? Tell them. Pass this along. This kind of info saves lives.

The deeper issue here isn't just formularies or tiers-it's the commodification of health. When a life-saving drug becomes a product subject to market forces, we've lost something essential. The fact that a $100,000/year drug can be excluded from coverage while ibuprofen is free speaks to a moral failure. The $2,000 cap is a step, but we must demand universal access. Not negotiation. Not tiers. Not prior auth. Just access.

As someone in South Africa, I can't even imagine the complexity of this. We have no formularies-just scarcity. But I’ve seen people pay $100 for a month's supply of hypertension meds. The irony? In the U.S., you have choices. In many places, you have none. This guide? It’s a luxury. And yet-you’re still fighting. Respect.

The fact that one must consult a pharmacologist to navigate insurance tiers is not innovation-it is systemic failure. One cannot reasonably expect laypersons to decode opaque contractual structures designed by actuaries to maximize profit. This is not healthcare. It is financial engineering disguised as social welfare.